Are you considering starting a new business or expanding your existing one? If so, you’ll likely hear about business loans – and for good reason! It is an important capital that helps small businesses get off the ground, expand their operations, and even manage day to day finances.

You must understand what a business loan is and its different types to figure out which one might be right for your business goals. In this guide, we’ll break down what a business loan is. And how you can get one.

Understanding Business Loans?

If you want to take a loan for your business, you must know what a Business Loan is. The business loan is a funding source to offers loans to small businesses for multiple purposes. You can use these funds to support your business’s processes, expansion, equipment buying, or inventory purchasing. When you take out a loan, the lender lends an amount of funds, and you both agree on the terms and conditions for repayment. The agreement includes details of interest rates and repayment duration. Always remember that loans are customized with different interest rates and repayment schedules on the basis of your business’s credit rating. The capitals are important for your business expansion, asset investment, and cash flow management. They also help to overcome your financial obstacles.

Secured and Unsecured Loans

Secured Business Loans

In secured business loans, the borrower offers collateral in addition to a personal guarantee to back the loan. The collateral can be real estate or machinery. The assets that the borrowers provide present a security to the lender.

Unsecured Business Loans

The unsecured business loans are different from the secured loans, and they do not require any collateral from the business. In an unsecured business loan, lenders assess factors to approve the loan. The lender considers the operating duration of the company and its financial stability. They also assess the cash flow of the small business before they approve the loan.

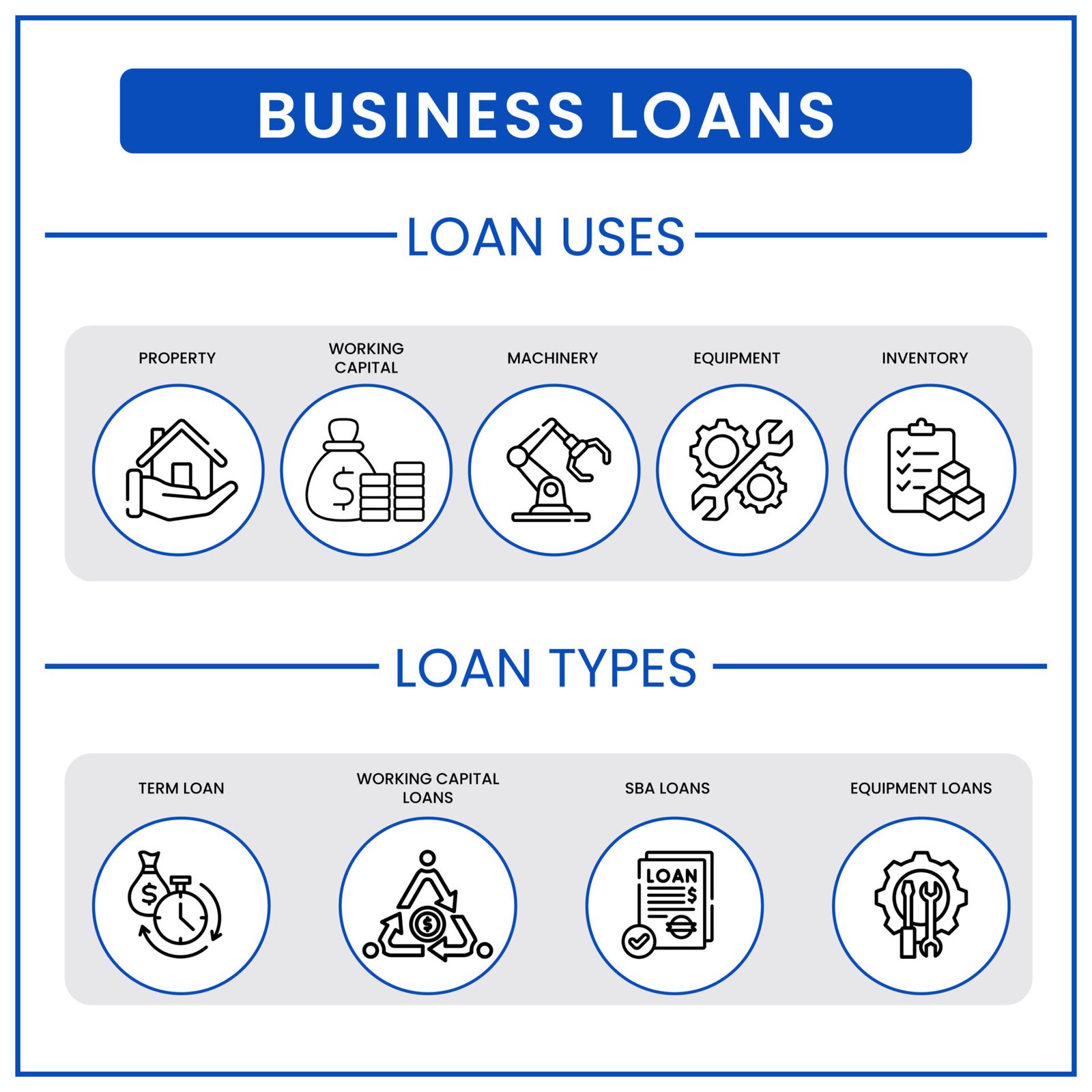

Types Of Business Loans

The business loans are of different types with multiple purposes.

Term Loan

The term business loans for startups is a popular funding choice for small businesses. This type of loan is for borrowers who want a total amount with a set repayment schedule. A term loan comes with flexibility, and the loan can provide financing to multiple initiatives. Term loans can finance equipment buying, business expansion, and operational capital. Borrowers receive the full loan amount upfront and repay it over a predetermined duration. The duration is often between one to ten years. The interest rates for these business loans are either fixed or variable. It depends on the lender and the borrower’s credit profile. A term loan gives steady payments. The businesses can manage money and work toward long term goals.

SBA Loans

The business loans for startups that the Small Business Administration (SBA) provides are called SBA Loans. The loan has favorable interest rates and extended repayment timelines. The Small Business Administration itself doesn’t lend money, instead, it guarantees a portion of loans. Commercial lenders make this portion to small businesses, which are banks and credit unions. The guarantee decreases the risk for lenders, and they feel more confident to offer funds to small businesses that might not otherwise qualify for traditional loans.

Working Capital Loans

These business loans address the short-term financing needs and cover daily operational expenses. The working capital loans are for inventory purchases, payroll, rent, or other immediate cash flow requirements. They are different from the long-term loan. The repayment periods for the working capital loans are shorter and range from a few months to a few years. They help businesses cover short-term cash needs and continue operations. Businesses need a working capital loan if they want to continue their operations and take advantage of expansion prospects in evolving market conditions.

For lenders, we provide working capital leads. These leads are the merchants who are actively looking for business loans to improve their business.

Startup Loan

Startup loans are a financial lifeline for nascent businesses. This business loan for startups presents the initial capital necessary to change creative ideas into successful enterprises. Startups lack the great financial history or significant collateral that traditional lenders require. They are not like the companies that have proven track records. Therefore, startup loans bridge this gap. They offer a loan for important early-stage needs. The early-stage needs include:

- Product Development

- Market Research

- Initial Inventory

- Operational Expenses

- Office Space

Different sources, like government programs, angel investors, venture capitalists, or crowdfunding, can provide these loans. Each option has its own rules, interest rates, and benefits to support the needs and growth of new businesses.

Equipment Loans

Equipment loans help businesses to purchase necessary machinery, vehicles, technology, or other fixed assets without using their working capital. The business buys the equipment, which then serves as collateral for the loan. The equipment loans have lower interest rates and better repayment terms than unsecured loans. Lenders consider the lifespan and resale value of the equipment when they determine the loan’s duration and terms. It helps businesses to align their loan payments with the asset’s useful life.

Other Types Of Business Loans

There are some unusual types of loans also. Businesses have the opportunity to explore the multiple types of loans and select the one that matches their needs.

Invoice Factoring or Invoice Financing Loans

Businesses that require quick cash flow but are awaiting client payments can use the solutions. A company can sell or borrow against its outstanding invoices to a third-party lender rather than waiting for payments. This offers rapid liquidity, but frequently at a cost or discount. This provides quick liquidity, though often at a discount or fee.

Real Estate Business Loans

The loan is for the acquisition and construction. It is also for the refinancing of commercial properties. They are long term loans, and real estate itself secures them. Businesses that want to own their premises and expand their physical footprint can take this loan.

Microloans

Microloans are small-dollar loans. They range from a few hundred to tens of thousands of dollars. The loans are for startups or very small businesses that might not qualify for traditional bank loans.

Merchant Cash Advance (MCA)

Technically, this is an advance on future credit and debit card sales for a business rather than a loan. Up until the advance plus a fee is paid back, a lump sum is given upfront, and repayment is made using a percentage of daily credit card transactions. Although Merchant cash advances provide extremely quick access to capital, their effective interest rates are usually high.

Franchise Loans

These business loans help individuals or businesses finance the purchase or development of a franchise. The lenders who offer these loans know about the franchise model. They may consider the strength of the franchisor’s brand and business plan when they assess the eligibility. The franchise loans have favorable terms due to the established nature of many franchise systems.

What are Business Loans Used For?

The borrowers use business loans for a variety of different purposes:

- Business property acquisition or renovation

- Working capital for routine expenditures

- Liability merging or reloaning

- Machinery acquisition

- Stock acquisition

- Firm buyouts or enlargement

- Funding initial expenses

- Franchise agreement acquisition

- Promotional activities and publicity

Tip: You can sometimes use one business loan to pay off another business loan. This may make financial sense if by refinancing, you get a better interest rate than that charged for your original loan.

What are the Benefits Of a Business Loan?

The loans offer small businesses the funds that they can use in their growth and development. The small business owners can expand their business operations and earn more returns with the business loan. The companies can make more profit with the help of funding capital. Business loans have lower interest rates and longer repayment periods than other options, like credit cards. The business loan also has the option of fixed or adjustable interest rates. There are multiple repayment choices for the business loan.

How Do You Qualify For a Business Loan?

The business loan lenders have particular criteria to see if the borrower qualifies for the business loan or not. The main aspects of this criterion are:

- Creditworthiness

Lenders assess both your personal and business credit scores to gauge your debt management history.

- Time In Business

The lenders also see how much time the small business spends in the business industry. Lenders often prefer businesses with a track record (e.g., 1-2+ years) for stability.

- Revenue & Cash Flow

The revenue and cash flow are also important aspects of the qualifying criteria. Sufficient annual revenue and consistent positive cash flow demonstrate your capacity to make payments.

- Collateral

The assets reduce lender risk and secure better terms. The assets, like property or equipment, are good for secured loans.

- Business Plan & Loan Purpose

The debtor also needs to provide a clear plan that outlines how the loan will be used for growth or operations. The plan adds value to the application of the borrower and increases their chances of qualifying.

- Debt Ratios

Lenders check borrowers’ existing debt burden to make sure they can handle additional financing.

In order to support their application, the loanee should also prepare bank statements, tax returns, and financial statements.

FAQs

Can I Use a Personal Loan for My Business?

Yes, you can use a personal loan for your business. If you take out a personal loan for your business means you’re personally responsible for the debt. It’s easier to get than a business loan, but it won’t build business credit and could put your assets at risk. Always keep finances separate and talk to a financial advisor before deciding.

Can You Have More Than One Business Loan?

Yes, a business can take more than one loan at a time. The practice is called loan stacking. While it provides more capital, it also increases repayment pressure, costs, and credit risk. Careful financial planning and honest communication with lenders are important for loan stacking.

What Happens If My Business Cannot Pay Back a Loan?

The first missed payments of a loan will result in delinquency, which will affect your credit scores, incur late fees, and make future financing challenging if your company is unable to repay it. If you don’t fix missed loan payments, the lender may declare a default and demand full repayment. They can take your assets, sue you, or send the debt to a collection agency. In the worst case, you might have to file for bankruptcy.